Three Things We’re Hearing

- Cap One and Disco shake things up!!

- Your competition is benchmarking… and you should too!

- SoFi leads the way on personal loans

A four-minute read

If you would like the Epic Report delivered right to your inbox, click here

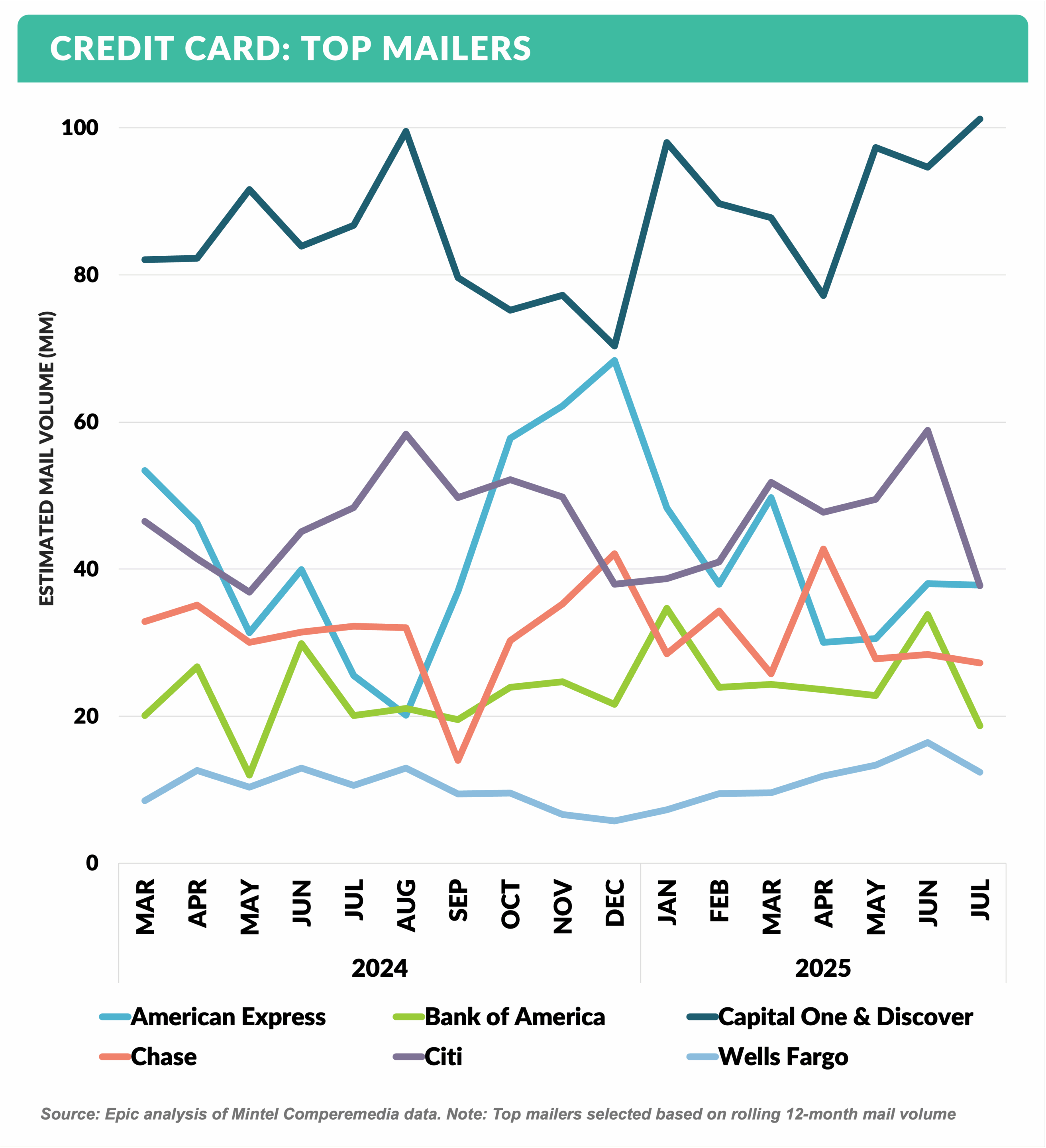

Cap One and Disco Shake Things Up!!

- Capital One completed its acquisition of Discover in May, and, while much attention has been focused on Capital One’s access to the Discover network, the merger will have a dramatic impact on consumer lending

- Credit Cards

- Pre-combination Cap One and Disco were among the most dominant card marketers, with Capital One mailing ~50+ million pieces per month and Discover ~30+ million in the 12 months ending May ’25 — a combined volume of 80 million

- In the first full post-merger month, July saw a 25% jump to over 100 million pieces for the combined entity

- With a combined card portfolio exceeding $250 billion, and assuming a natural attrition rate of a (probably low) 15%, Capital One will need to acquire close to $40 billion in new receivables per year just to remain flat (as a point of reference, number 8 issuer Wells Fargo has ~$50 billion in loans and number 9 Barclays just under $40 billion)

- Home Equity

- Following the finalization of the merger in May, Capital One announced that it was discontinuing the origination of home equity loans

- Up until the companies’ combination, Discover had been the number one mailer of home equity products

- This market void will present an additional opportunity for other lenders in the home equity market, as pointed out in the July Epic Report, as lenders have not kept up with the growth of total home equity which now exceeds $35 trillion

- Student Lending

- In July ’24, prior to the completion of the merger, Discover sold their student lending portfolio to private equity firms KKR and Carlyle, and, while not directly attributed to the merger, its effect on the student lending market is significant

- Neither Discover nor the purchasers continued new loan originations in this market where Discover had been a leader and the number one mail marketer

- Discover’s 2024 exit was immediately noticed in the 2024 “peak season.” However, much of that shortfall has since been filled in by College Ave, Sallie Mae, and Citizens with 2025 volume up 76% through July

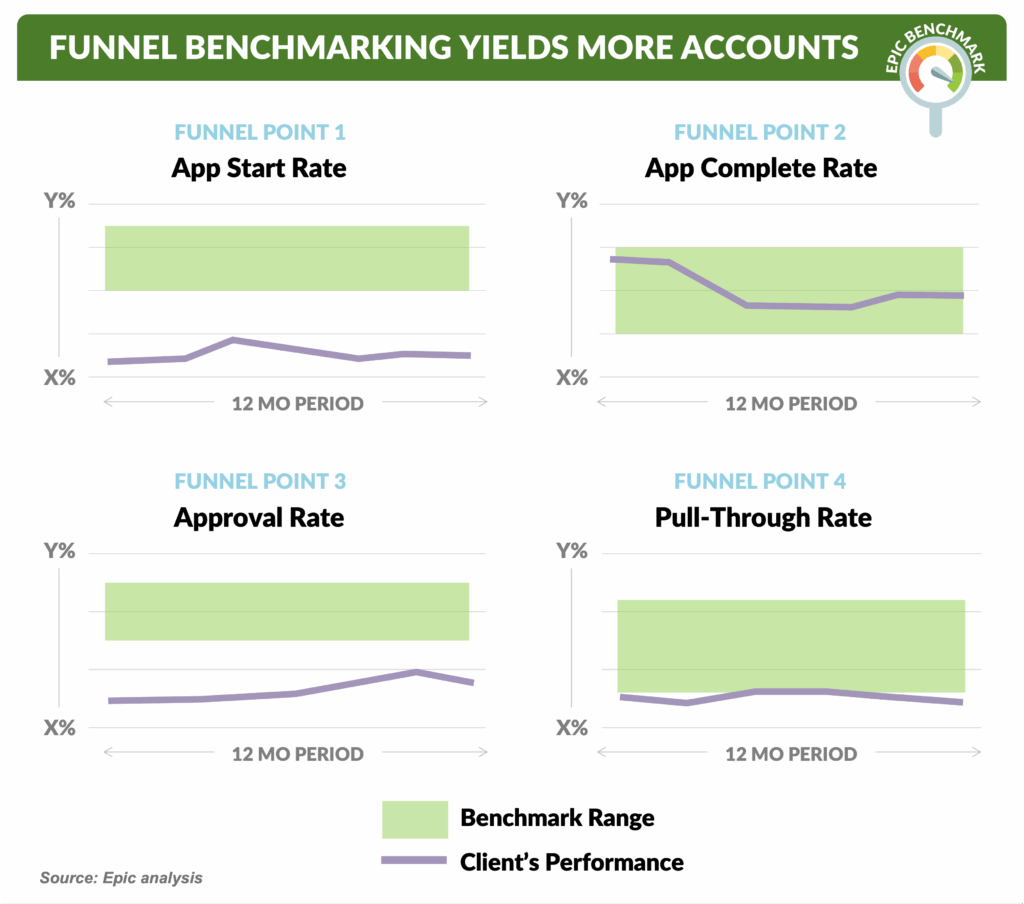

Your Competition is Benchmarking and You Should Too!!

- The most effective marketing today is faster to market, smarter in execution, and optimized against competitive benchmarks

- In the direct mail channel, the cost per piece mailed (CPP) is, along with net response rate, one of the key drivers of acquisition cost

- Leveraging our benchmarks and expertise with supplier negotiations, clients regularly uncover significant cost savings across the four major CPP components — print, postage, bureau, and data

- Another leverage point for marketers is shortening cycle times, allowing evolving insights to shape decisions more quickly

- Benchmarking against best-in-class timelines can help marketers cut cycle times by 30%, creating a decisive speed-to-market advantage

- Product design is another area with material possibilities for increased profitability — an analysis of your product set as it lines up to your target market and competitive products can optimize marketing spending and profitability

- Channel spend and mail volume analyses show competitor focus — insights you can use to sharpen strategies and justify budgets

- Marketing impact isn’t just about who you reach and how — it’s also about optimizing the journey from application start to successfully-booked account

- By benchmarking funnel metrics — such as application starts, completions, approvals, and pull-through — clients drive smarter, more efficient volume through every stage

- A review of competitor customer journeys can identify best-in-class experiences that strengthen engagement and profitable behaviors

- By combining benchmarking and competitive insights across all profit drivers, we’ve helped clients capture tens of millions of dollars in savings and performance gains

- Contact us to see how Epic can help you develop an industry leading direct marketing program

SoFi Leads the Way on Personal Loans!

- Spending on home equity marketing is significantly higher than YTD ’24, with Discover’s lost volume likely to impact this trend going forward

- Continuing a 12-month trend, SoFi’s July personal loan mail volume more than doubled that of its nearest competitor Upstart

- Since peaking in late 2023 around 4.5%, average rates for high yield savings accounts began trending down in late-2024 and have recently plateaued at 3.75%

- Demand for deposits has softened for banks as loan growth has leveled off

- We’ve noted the reluctance of commercial banks to participate in personal loan lending, often due to concerns about credit. However, delinquency on personal loans has actually been stable over the past three years as balances have grown by one-third

- The grocery industry is witnessing a significant shift in payment preferences as more consumers turn to buy now, pay later (BNPL) services to manage their food shopping expenses amid persistent inflation

- According to a recent LendingTree consumer survey, 25% of BNPL users have utilized these services for grocery purchases — a dramatic increase from just 14% a year ago

- Costco recently introduced its own BNPL option, partnering with payment network Affirm to offer customers the flexibility to spread grocery costs over time, often with zero interest for qualifying purchases

Thank you for reading.

Jim Stewart and Ben Brake

www.epicresearch.net

The Epic Report is published monthly, with the next issue in October.

Do you have a question about this issue or a suggestion about a future Epic Report topic? Please email us with your comments and suggestions on future topics or to have someone added to our distribution list.

Epic Research is a marketing company that helps our financial services clients acquire new customers via organic growth. Reach out if we can help you achieve world class results!