Three Things We’re Hearing

- Direct mail’s advantage over digital marketing

- Huge opportunity in education refi!

- Personal lending originations soar!

A four-minute read

If you would like the Epic Report delivered right to your inbox, click here

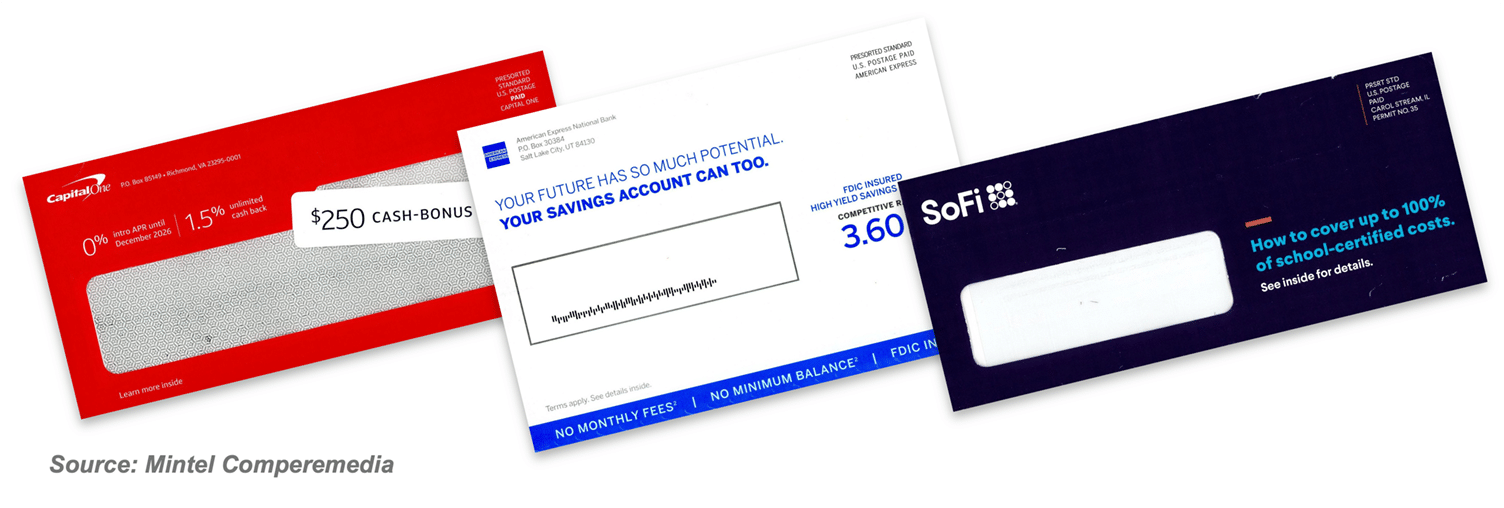

Direct Mail’s Advantage Over Digital Marketing

- Today, as has been the case over the past four decades, we’re often met with skepticism from those outside of the consumer finance industry when talking about the effectiveness of direct mail in generating new customer relationships

- There are several reasons mail still works — including today’s less cluttered mailboxes and the ability to drive significant volume through credit bureau extracts — but a more recent benefit is that in an age of AI-generated ads and synthetic content, physical mail’s tangibility offers financial brands a reliable platform for delivering marketing messages with confidence and clarity

- Physical mail conveys “this is real” in a way digital can’t always replicate and, even with expanding digital capabilities, direct mail continues to command acquisition spend — accounting for 71% of Credit Card, 59% of Deposits and 86% of Lending spend last year, consistent with years prior

- Many of the largest financial mailers build credibility and authenticity through creative techniques like personalization, testimonials, trust-badges, and tactile treatments

- When direct mail personalization is specific and insightful, consumers infer real data and real oversight, invoking trust

- This Figure HELOC mail package uses estimated market value and equity in your home to make the offer feel tailored and credible

- The Citi® / AAdvantage® Platinum Select card uses personalized miles balance data to make the offer feel valuable and tangible

- Consumers are looking for verification — not just claims — and direct mail formats provide real estate to build this credibility

- Earnest surrounds the call-to-action area of this education refinance offer with testimonials and third-party trust ratings to reduce uncertainty around a significant financial decision

- Personal loan lender Best Egg displays multiple trust badges — BBB A+, Trustpilot and their own “Be Money Confident” logo — to signal legitimacy and reduce perceived risk

- Capitalizing on physical touch can drive engagement and response

- Capital One’s longstanding tip-on card format remains a standout example — mimicking the feel of a real credit card and serving as a standalone application tool

- Other tactile and interactive treatments, like embossing on an envelope to make it feel different when the recipient flips through their stack of mail, can help boost engagement and may also help your mail qualify for valuable USPS postage incentives

- Why this matters for financial marketers: as AI accelerates and digital trust evolves, direct mail offers a grounded experience for financial communication — and we believe it will remain uniquely positioned as a workhorse channel in the years ahead

Huge Opportunity in the Education Refinance Sector

- Education refinance lending is a niche segment dominated by a few lenders, with SoFi and Earnest/Navient marketing most consistently, and Citizens recently returning to marketing

- Education refinance direct mail marketing remains a fraction of what it was six years ago due to the effects of Covid-era federal student loan payment deferrals and rising rates

- This low marketing volume compared to online search volume for “Education Refinance” suggests there is an ongoing gap between supply and demand

- Refi lenders are reinvigorating the category with bold marketing promises and urgent messaging as rates have finally begun to move lower

- SoFi in particular has demonstrated how nimble they can be in adjusting rates, emailing consumers about new lower rates within 100 minutes of the Fed’s December rate drop

- Aside from rate messaging, student loan refi marketers continue to promote an easy application experience, rate checks with no credit score impact, and no fees as ways to entice consumers

- Lenders also seek to personalize their messages using humans — real and AI — to promote the benefits of refinancing

- As rates continue to decline, the education refinance market should heat up

- Many people holding debt from student loans issued in the last few years are sitting on rates significantly higher than the 4.5%–5% refinance rates

- For borrowers who graduated between 2023 and 2026, the average weighted fixed interest rate across their portfolio is likely between 6.5% and 8%, making them prime candidates for a 5% refinance loan

Personal Loan Originations Soar

- Personal loan originations in 2025 are over 27% higher than 2024, with fintechs accounting for ~41% of the volume vs ~32% a year ago

- Total industry balances for personal loan are now above pre-Covid levels, as some commercial banks have re-entered the market and fintechs increase marketing spending

- Credit card direct mail volume has been steady since the late 2021 post-Covid recovery — ranging between 300 – 400 million pieces per month — however, consumer search volume has tailed off in the past two years

- JPMorgan will take over issuance of the Apple Credit Card from Goldman Sachs

- Goldman Sachs launched the Apple Card in 2019 to immediate consumer success, but the partnership has recently struggled with profitability, leading Apple to begin seeking a new issuer in 2023

- JPMorgan is buying the portfolio at a $1 billion discount – card portfolios typically trade at premiums closer to 10%

- JPMorgan is currently the second-largest card issuer in the U.S. with roughly $210 billion in outstanding loans and after acquiring Apple’s estimated $20 billion portfolio, would tighten the gap between JPMorgan and the new market leader, Capital One, which commands approximately $250 billion in loans following its merger with Discover

- 60% of consumers believe monitoring their credit is “extremely or very” important, with over half of them checking at least monthly

- PayPal submitted an application to create an Industrial Loan Company (ILC) bank charter in Utah

- ILCs are limited in what they can do compared to traditional banks, but offer a unique "loophole" that allows commercial firms (like retail or tech companies) to own a bank without becoming a Bank Holding Company

- If approved, the ILC will allow PayPal to increase its profit margins in a few specific and already-scaled-up product areas (it has done roughly $30 billion worth of small business lending since 2013) while giving itself more optionality for the future, such as offering their own high yield savings accounts

- Recent federal legislation eliminated Graduate PLUS student loans for new borrowers and caps Parent PLUS loans at $20,000/year

- This loss will create a significant "funding gap" for high-cost degrees, substantially increasing demand for private student loans

- The elimination of these federal loans is expected to benefit private lenders such as Sallie Mae, College Ave, and Citizens, increasing the annual market for new private loans from an estimated $13 billion per year to over $20 billion

Thank you for reading.

Jim Stewart and Ben Brake

www.epicresearch.net

The Epic Report is published monthly, with the next issue in February.

Do you have a question about this issue or a suggestion about a future Epic Report topic? Please email me with your comments and suggestions on future topics or to have someone added to our distribution list.

Epic Research is a marketing company that helps our financial services clients acquire new customers via organic growth. Reach out if we can help you achieve world class results!